What are Net Identifiable Assets?

Attorneys with you, every step of the way

Count on our vetted network of attorneys for guidance — no hourly charges, no office visits.

2000+

businesses

Helping entrepreneurs turn ideas into

businesses over 2000+ times in Russia.

1500+

consultations

Providing access to our independent

network of attorneys over 1500 times.

90+

liquidations

Helping companies to close down operations in the smooth way

Net Identifiable Assets, in the context of M&A, refer to the fair value of an acquisition target’s assets once the corresponding liabilities have been deducted. by the target company.

How to Calculate Net Identifiable Assets

Net identifiable assets (NIA) are defined as the total value of a company’s assets net of the value of its liabilities.

Identifiable assets and liabilities are those that can be identified with a certain value at a specific point in time (and with quantifiable future benefits/losses).

More specifically, the NIA metric represents the book value of assets belonging to an acquired company once liabilities have been subtracted.

It is important to note that the terms:

- “Net” means that all identifiable liabilities as part of the acquisition are accounted for

- “Identifiable” implies that both tangible assets (e.g. PP&E) and intangible (e.g. patents) can be included

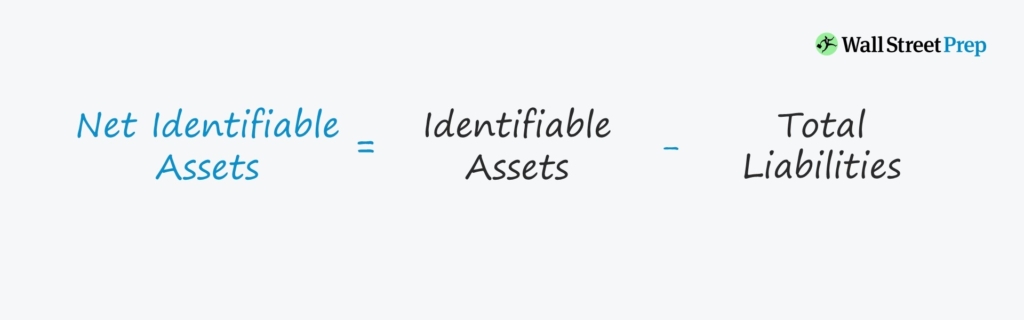

Net Identifiable Assets Formula

The formula to calculate a company’s net identifiable assets is as follows.

Formula

- Net Identifiable Assets = Identifiable Assets – Total Liabilities

Goodwill and Net Identifiable Assets

The value of a target’s assets and liabilities is assigned a fair value post-acquisition, with the net amount subtracted from the purchase price and the residual value recorded as goodwill on the balance sheet.

The premium paid over the value of the target’s NIA is captured by the goodwill line item on the balance sheet (i.e. excess over purchase price).

The value of goodwill as recognized on the books of the acquirer remains constant unless the goodwill is deemed to be impaired (i.e. the buyer overpaid for assets).

Goodwill is NOT an “identifiable” asset and is only recorded on the balance sheet post-acquisition for the accounting equation to remain true — i.e. assets = liabilities + equity.

Net Identifiable Assets Example Calculation

Suppose a company has recently acquired 100% of a target company for $200 million (i.e. asset acquisition).

In an asset acquisition, the target’s net assets are adjusted for both book and tax purposes, whereas in a stock acquisition, the net assets are written up for just book purposes.

- Property, Plant & Equipment = $100 million

- Patents = $10 million

- Inventory = $50 million

- Cash & Cash Equivalents = $20 million

The fair market value (FMV) of the target’s net identifiable assets on the date of the acquisition is $180 million.

Considering the FMV of the target’s NIA is greater than its book value (i.e. $200 million vs $180 million), the acquirer has paid $20 million in goodwill.

- Goodwill = $200 million – $180 million = $20 million

The $20 million is recorded on the balance sheet of the acquirer because the acquisition price exceeds the value of the net identifiable assets.